The EU Platform on Sustainable Finance’s reporting on data and usability of the EU taxonomy (October 2022) is based on maintaining the drive for sustainability in companies. To assess and encourage the EU’s sustainability goals, and to define what is meant by sustainable activities, the EU has created a “green” taxonomy. Since Europe is gradually requiring enterprises to provide an assessment of their capital expenditure and business activities as aligned with this taxonomy, it is significant to comprehend the green taxonomy and to understand if your company is obliged to report.

Framework

The framework of the EU green taxonomy reporting is aimed to contribute to the EU’s environmental objectives and to not do “ significant harm to any of the environmental objects”. In general, this means that for meeting the EU’s climate and energy targets for 2030 and to reach the objectives of the European green deal, it is necessary to direct investments towards sustainable projects and activities. Therefore, the EU taxonomy could provide “investors with security, protect private investors from greenwashing, help companies to become more climate-friendly, mitigate market fragmentation and help shift investments where they are most needed”. Furthermore, “the EU taxonomy does not only specify disclosures but also mandates the usage of the resultant data”.

For a company to be on par with the taxonomy, the business activity should be carried out in compliance with “any minimum safeguards” (e.g. UN Guiding Principles on Business and Human Rights), and with industry standards which can be classified as a set of technical screening criteria.

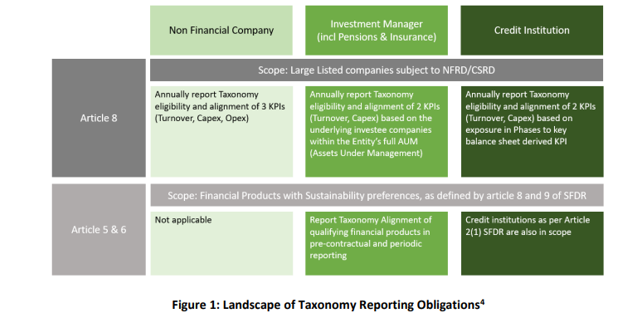

The green taxonomy is not an XBRL taxonomy, but rather a classification system for sustainability reporting. Herein, various (economic) activities are categorised by their impact on the EU environmental objectives. To assist the EU in measuring, and therefore meeting, these goals, the companies should disclose the following information as indicated in the taxonomy: operational expenditure, turnover, and capital expenditure. Article 8 disclosure is utilized as legislation specifying the disclosure rules for both financial and non-financial companies. For an overarching overview of reporting obligations, see figure 1.

Advantages

Not only EU’s sustainability goals can be assessed with the information from the green taxonomy, but the data can help inform investors since the legislation requires financial companies to use the data as reported by non-financial companies in assessing the sustainability of said enterprise’s investments. Moreover, the data can be of interest to the European Supervisory Authorities which include European Securities and Markets Authority (ESMA), European Banking Authority (EBA), and European Insurance and Occupational Pensions Authority (EIOPA). According to CoreFiling, the resulting is optimal to share broadly and efficiently and to create “digital, machine-readable and standardise reporting”.

Noticeable is that, whilst the legislation is showing the reported data, a digital data standard is still lacking. Concerns are that, potentially, the burden of the legislation on companies gets increased and that third parties or national variations can fill this gap. The expectation is that the EU will require disclosures in Inline XBRL (iXBRL), which is an extension of the European Single Electronic Format (ESEF).

Concept of Proof

In a concept of proof by the collaboration between CoreFilign and Greenomy, an XBRL standard is created for the company and regulatory reporting. In this IXBRL document, the proof of concept was successful and article 8 in the EU taxonomy legislation could be produced, applied, and tagged. The report and the interactive version of the green taxonomy can be found here.

Conclusion

To conclude, “legislators can reduce the burden of data-focussed legislation by mandating digital, machine-readable and standardised data definitions and reporting formats”, as seen in the IXBRL concept of proof. By creating a human and computer-readable document, the sustainable activity taxonomy can be effortlessly shared, digitalised, and standardised. This would assist in reducing the efforts of the company, and give no rise to a gap in the reporting procedure. In general, the EU green taxonomy benefits not only the outlook on the EU ‘s sustainability goals but also on “any jurisdiction where a flow of data among market participants is required to meet sustainability goals”. Concerning companies, having a positive outcome on the EU green taxonomy can rake in investments to further emphasise and meet the sustainability goals.

The document of Platform on Sustainability Finance’s recommendations on data and usability of the EU taxonomy can be found here.

Sources

https://www.xbrl.org/news/digitising-the-eus-green-taxonomy-a-proof-of-concept/

https://www.corefiling.com/2022/10/20/digitising-the-eu-taxonomy/

https://www.nordea.com/en/news/the-final-eu-taxonomy-and-next-steps-in-sustainable-finance-0